For a company that is currently selecting materials for plastic packaging for the European market, PPWR is not just a matter of what the law requires. It is a matter of what risk profile the chosen material carries looking ahead to 2030—and who bears that risk.

PP and PET are both well-established materials for food packaging. However, under the PPWR, the two materials are in very different positions. PP is subject to a lower recycling requirement, has four documented compliance pathways, and is covered by the regulation’s derogation provision. PET faces a requirement three times higher by 2030, has effectively only one unconditionally approved compliance pathway today, and is explicitly excluded from the safety valve that PP can activate in the event of a supply disruption.

This article compares the regulatory and supply situations for PP and PET under the PPWR. The requirements for recycled content by material type are described in Recycled Content in Plastic Packaging Under the PPWR—Requirements, Timeline, and Material Differences. The supply market for rPET is reviewed in The rPET Market in Europe

Two materials, two different regulatory profiles

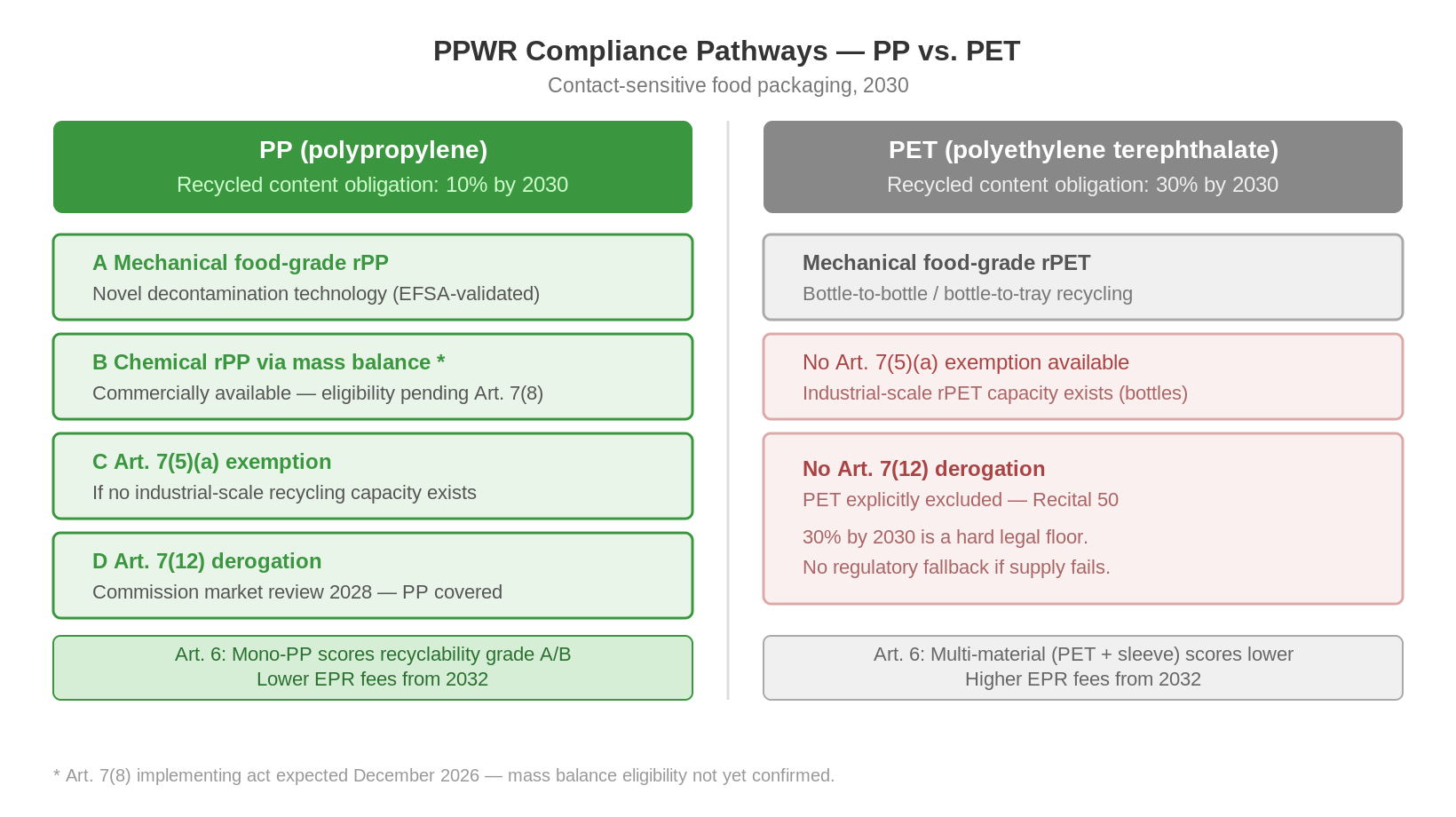

The starting point is the requirements set forth in Article 7. For PET packaging that comes into contact with food, the requirement is 30% post-consumer recycled content starting in 2030, rising to 50% in 2040. For PP, the requirement is 10% starting in 2030 and 25% starting in 2040. The difference is not marginal—the PET requirement is three times that of PP in 2030 for the same type of contact-sensitive packaging.

But the asymmetry does not stop at the threshold levels. It continues in the regulation’s framework for what happens if the market cannot deliver. Article 7(12) allows the Commission to postpone the compliance deadline for PP and other non-PET plastic types based on a market review in 2028. PET is explicitly exempt from this provision—not as an oversight, but as a deliberate legislative choice articulated in Recital 50. For a packaging buyer, the implication is simple: PP has a fallback; PET does not.

In addition, under Article 7(5)(a), PP may seek an exemption from the requirement if there is no industrial recycling capacity on a sufficient scale. This exemption does not apply to PET—there is industrial recycling capacity for PET bottles, and the Commission has determined that the market can supply the required volume.

PP’s Four Paths to Compliance by 2030

PP’s regulatory profile is not only favorable in terms of the threshold level—it is favorable because PP has four documented ways to meet its obligations.

The first approach involves mechanically recycled food-grade PP produced using newly developed super-purification technology. The technology has been validated by EFSA and is commercially available—though not yet on an industrial scale for all European markets. European development initiatives in the field of mechanically recycled food-grade rPP are currently being scaled up.

The second route is chemically recycled PP via mass balance allocation. Processes based on the pyrolysis of plastic waste can currently supply rPP through certification schemes such as ISCC+. The material is commercially available. Whether it qualifies as post-consumer recycled content under the PPWR will be determined by the implementing act under Article 7(8), which is expected in December 2026.

The third option is the exception under Article 7(5)(a): if there is no industrial recycling capacity for food-grade rPP on a sufficient scale, the manufacturer may apply for an exemption by providing supporting documentation. This provision is specifically designed for situations such as that of PP today—a material with a growing recycling ecosystem, but not yet at an industrial scale.

The fourth option is the safety valves provided for in Article 7(12) and 7(13): the Commission’s ability to defer the requirement for PP based on the 2028 market review, and the general emergency clauses that can be activated in the event of documented supply crises.

PET’s Supply Challenge: One Path, One Market

PET’s compliance framework is simpler than PP’s—and more vulnerable. The path to 30% rPET by 2030 lies primarily in the mechanical recycling of collected PET into food-grade rPET. This is the only route that is currently unconditionally approved under the PPWR.

The challenge is that this market is under pressure. According to data from Plastics Recyclers Europe (PRE), the European PET recycling industry shut down 300,000 metric tons of capacity in 2024—the largest capacity reduction ever—as a result of pressure from cheap imported rPET pellets and falling virgin PET prices. PRE identifies food-contact rPET as the segment under the most pressure and emphasizes that the approximately 6% annual capacity growth needed to meet PPWR requirements is not currently underway.

In addition, there is structural competition for the limited food-grade rPET capacity. PET bottles are subject to the SUP (Single-Use Plastics) Directive, which requires 25% rPET in PET beverage bottles starting in 2025 and 30% starting in 2030. Bottle manufacturers and tray manufacturers compete for the same supply source. For non-bottle PET packaging—including trays and cups—specific recycling capacity accounts for less than 3% of total European PET recycling capacity, according to available market data.

The regulatory asymmetry in Article 7(12)

The most underestimated aspect of the integration of PP and PET in a PPWR is not the threshold level—it is what happens in the event of a supply failure.

Article 7(12) stipulates that the Commission must conduct a market review by 2028 at the latest and, based on that review, may decide to postpone the compliance date for specific material categories if insufficient supply capacity is demonstrated. PP and other non-PET plastic types are covered by this provision.

PET is exempt. Recital 50 states that the legislature has actively chosen to exempt PET from the derogation mechanism because the existing recycling ecosystem for PET bottles is considered sufficient to support the obligation. This is a risk assessment made by the legislature—not a guarantee that the market will be able to deliver.

The practical implication is that, for a brand owner who has opted for PET by 2030, the 30% requirement is the legal minimum. There is no fallback provision in the text of the regulation. Security of supply is a commercial issue, not a regulatory safeguard. For PP, regulatory flexibility is built into the framework.

Design for Reuse: Single-Material vs. Multi-Material

In addition to the requirements for recycled content under Article 7, the PPWR introduces a parallel dimension in Article 6: design for reuse and recyclability grades, which, starting in 2030, will classify packaging from A to D based on its suitability for reuse, and which, starting in 2032, will modulate EPR fees.

Monomaterial designs—a single type of plastic without secondary material layers—generally score higher on the recyclability scale than multimaterial designs. A monomaterial injection-molded PP cup is designed for direct entry into the PP recycling stream and, in accordance with the regulation’s design principles, will qualify for Grade A or B.

Multi-material solutions—including PET trays or cups with attached cardboard sleeves—are designs that, within the European sorting infrastructure, typically either require manual separation or are sorted together, and thus do not contribute effectively to either PET or paper recycling. This design does not reduce the mandatory requirements for PET content: the PET container is still subject to the 30% rPET requirement regardless of the attached cardboard layer. And under the EPR framework starting in 2032, the multi-material design will most likely score lower and incur higher fees than a comparable single-material solution. Multimaterial packaging and PPWR.

Summary

Under the PPWR, PP and PET are in significantly different regulatory positions leading up to 2030. PET is subject to the 30% requirement for post-consumer recycled content starting in 2030—three times PP’s 10% requirement—and is explicitly excluded from the Article 7(12) derogation mechanism. PP has four documented compliance pathways: mechanical food-grade rPP, chemical rPP via mass balance (subject to the Article 7(8) decision in December 2026), the exemption option under Article 7(5)(a), and the safety valves under Article 7(12) and 7(13). PET currently has, in effect, only one unconditionally approved pathway: mechanical recycling into food-grade rPET—in a market that is contracting and competing internally for limited capacity. Chemical recycling of PET (depolymerization) exists but, like chemical rPP, is awaiting the Article 7(8) decision on mass balance. In addition, monomaterial PP structures score higher on design for recycling under Article 6 than multimaterial solutions, including PET+paper combination structures.

Frequently Asked Questions

No. For contact-sensitive packaging, the PET requirement is 30% post-consumer recycled content starting in 2030, compared to 10% for PP. The requirements are three times higher for PET in 2030 and twice as high in 2040.

Article 7(12) allows the Commission to extend the compliance deadline for PP and other non-PET plastic types based on a market review in 2028. PET is explicitly exempt from this provision under Recital 50. This is a deliberate legislative choice: PP has a regulatory fallback, while PET does not.

The four pathways are: (A) mechanical food-grade rPP via super-cleaning technology, (B) chemical rPP via mass balance allocation (pending a decision under Article 7(8) in December 2026), (C) an exemption under Article 7(5)(a) if industrial recycling capacity is lacking, and (D) the safety valves under Article 7(12) and 7(13).

It is uncertain. Plastics Recyclers Europe (PRE) documented the closure of 300,000 metric tons of capacity in 2024 and identifies food-contact rPET as the segment under the most pressure. Tray-specific capacity accounts for less than 3% of total European PET recycling capacity. Added to this is internal competition from bottle manufacturers subject to the SUP Directive’s requirement for 30% rPET by 2030. Multimaterial packaging and PPWR

Article 6 evaluates packaging based on its suitability for recycling within existing European sorting infrastructure. Single-material designs are directly compatible with single-material recycling streams and typically score a grade of A or B. Multi-material designs require separation for effective recycling and score lower—even though the cardboard layer does not affect the PET container’s rPET obligation under Article 7.