The rPET Market in Europe: Supply, Capacity, and Competition for Food-Grade Material

PET’s compliance path under the PPWR rests on a single assumption: that there will be sufficient food-grade recycled PET (rPET) available on the European market in 2030 to meet the 30% requirement in Article 7. This is a prerequisite that market data from 2024 and 2025 seriously call into question.

The European rPET market is not a single market—it is a hierarchy of applications with very unequal access to the limited supply of food-grade recycled material. PET bottles dominate the recycling infrastructure. Non-bottle applications—including trays, cups, and dairy product containers—are structurally at the bottom of this hierarchy as price takers in a contracting market.

This article describes the current state of the rPET market, the structural capacity constraints, and the competition for food-grade rPET resulting from the fact that two EU directives—the SUP Directive and the PPWR—impose simultaneous requirements on the same limited material stream. PP or PET by 2030? The regulatory and supply-side asymmetry.

The European rPET Market: Capacityand Structure

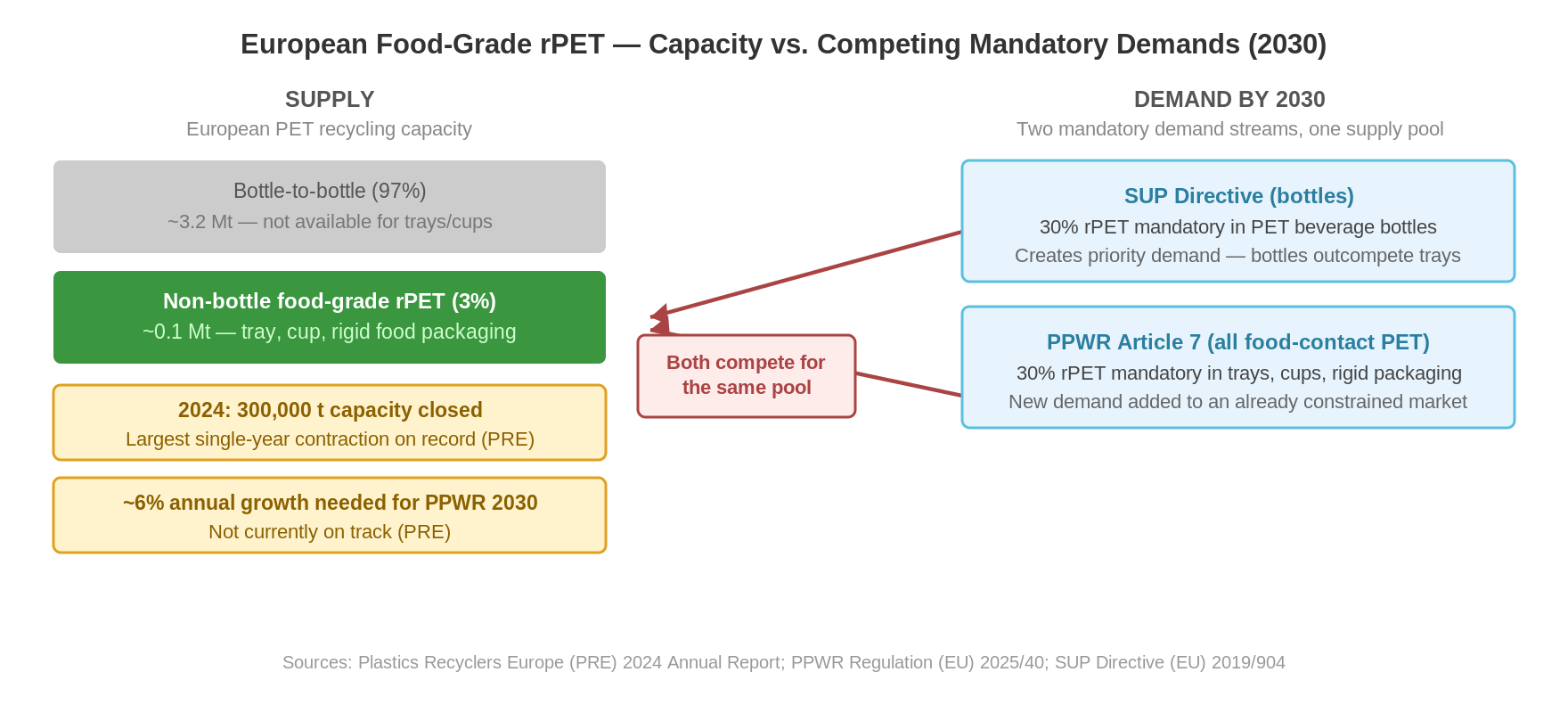

PET recycling in Europe is dominated by bottle recycling. Total European PET recycling capacity is estimated at approximately 3.3 million metric tons, the majority of which is configured to receive and process collected PET beverage bottles and convert them into food-grade rPET flakes or pellets for bottle production.

The capacity to produce food-grade rPET for non-bottle applications—including trays for dairy products, cups, bowls, and other rigid packaging—is estimated at less than 0.1 million metric tons, corresponding to less than 3% of total European capacity. The technology for producing food-grade rPET suitable for trays is well established, but the industrial infrastructure—sorting facilities configured for tray fractions and recycling plants with food-contact approval for tray input—is far more limited than the infrastructure for bottles.

The absence of a dedicated tray-to-tray recycling stream means that manufacturers of PET trays and cups are, in practice, competing for bottle-grade rPET that is remolded for tray applications. This is a market with lower efficiency and higher costs than the bottle-to-bottle stream—and one that is typically given lower priority when recycling facilities optimize for volume and margin.

Capacity Contraction and Market Signals

In 2024, the European PET recycling industry shut down capacity equivalent to approximately 300,000 metric tons—the largest single-year contraction since the industry’s inception. The cause was a combination of falling demand, import competition from cheaper rPET pellets from Asia, and lower virgin PET prices, which put pressure on rPET margins. The industry organization Plastics Recyclers Europe (PRE) reports a 5.5% decline in revenue for the European recycling industry as a whole.

PRE has identified food-contact rPET as the segment under the greatest pressure and has pointed out that the growth in recycling capacity needed to meet the PPWR’s 30% requirement by 2030 requires approximately 6% annual capacity growth—a level of growth that, according to PRE’s analyses, is not currently underway.

In March 2026, Indorama Ventures—one of Europe’s largest PET and rPET producers—declared force majeure on shipments, leading to subsequent shutdowns in preform production at dependent customers. This is a single incident, but it illustrates the vulnerability of a supply chain that is already under structural pressure.

Structural Competition: The SUP Directive Meets the PPWR

What makes the European rPET situation unique as we look toward 2030 is not only that capacity is limited—it is that two separate EU regulatory instruments impose simultaneous requirements on the same supply source.

The SUP Directive (Single-Use Plastics Directive) requires a 25% recycled content in PET beverage bottles starting in 2025, rising to 30% by 2030. This requirement specifically affects bottle manufacturers and creates structural, mandatory demand for food-grade rPET for bottle applications. Bottle manufacturers are actively purchasing rPET to meet SUP requirements—and they are willing to pay a premium for certified food-grade material.

Article 7 of the PPWR requires 30% rPET in all food-contact PET packaging starting in 2030—including trays, cups, and bowls that are not beverage bottles. This is a new and separate demand placed on the already limited food-grade rPET capacity. As a result, bottle manufacturers and tray/cup manufacturers are competing for material from the same recycling ecosystem. Bottle manufacturers are structurally better positioned in this competition: they purchase in higher volumes, they compete for a more standardized material, and they are driven by mandatory regulatory demand that gives them an incentive to pay above the spot price.

Contractual rPET Allocation and Supplier Risk

For a brand owner planning to use PET packaging that complies with rPET standards by 2030, it is not enough to simply know that the rPET market exists. The question is whether it is possible to secure a contract-based, documented supply arrangement that will last through 2030 and beyond.

The relevant questions to ask a potential rPET supplier are: Is the allocation for food-contact applications contractually specified and not merely indicative? What backup supply partners are available if the primary supplier experiences capacity shortages, price volatility, or force majeure? What is the supplier’s plan for Article 7 compliance—and is it contingent on the implementing act decisions under Article 7(8)?

Market signals from 2024 and 2026 suggest that the answers to these questions will, in many cases, reveal a shorter and more vulnerable supply chain than what appears on paper to be a straightforward compliance solution.

What the Market Says About PP

The rPET market situation is not directly relevant to PP packaging—there is not yet an established European market for food-grade rPP on an industrial scale. But it is precisely the absence of this market that triggers PP’s exemption under Article 7(5)(a): if there is no industrial recycling capacity, the manufacturer may seek an exemption. The challenge for PP is not a market under pressure—it is a market that has not yet been established, and for which the regulation explicitly allows time to develop.

For PET, the situation is the opposite: the market exists, the Commission has determined that it can meet the demand—and the exemption option under Article 7(5)(a) and the derogation mechanism under Article 7(12) are therefore not available for PET. The European rPET market is currently experiencing a period of contraction and competitive pressure, and it is within this market that PET packaging manufacturers must find their compliance solution leading up to 2030. PP or PET leading up to 2030? The regulatory and supply-side asymmetry.

Summary

The European rPET market is structurally dominated by bottle recycling, with less than 3% of total capacity dedicated to non-bottle food-contact applications. Plastics Recyclers Europe (PRE) documented the closure of 300,000 metric tons of capacity in 2024 and identified food-contact rPET as the segment under the most pressure. The capacity growth of approximately 6% annually required to meet the PPWR’s 2030 requirements has not yet begun. Added to this is structural competition from the SUP Directive’s simultaneous requirement for 30% rPET in PET beverage bottles starting in 2030—a mandatory demand that competes directly for the limited food-grade rPET capacity. For tray and cup manufacturers planning to use PET-based packaging, the security of the rPET supply is an active commercial and contractual issue—not a given prerequisite.

Frequently Asked Questions

The available industrial capacity for food-grade rPET suitable for trays is estimated at less than 0.1 million metric tons, corresponding to less than 3% of the total European PET recycling capacity of approximately 3.3 million metric tons. The majority of this capacity is configured for bottle-to-bottle recycling.

The European PET recycling industry shut down approximately 300,000 metric tons of capacity in 2024 due to a combination of import competition from cheaper Asian rPET, falling virgin PET prices that squeezed rPET margins, and reduced demand in a weak packaging market. PRE reports a 5.5% decline in revenue for the industry as a whole.

The SUP Directive requires 25% rPET in PET beverage bottles starting in 2025 and 30% starting in 2030. This creates mandatory, regulation-driven demand for food-grade rPET for bottles—a demand that competes directly with PPWR’s requirement for 30% rPET in all food-contact PET packaging starting in 2030, including trays and cups.

Tray and cup manufacturers are structurally at a competitive disadvantage in the race for food-grade rPET compared to bottle manufacturers. They are competing for a material that is primarily designed for bottle applications, in a shrinking market, and without the regulatory incentive that the SUP Directive provides to bottle manufacturers. Securing rPET allocations through contracts leading up to 2030 is an active business priority.

For PP, there is not yet an established European market for food-grade rPP on an industrial scale—and it is precisely this that triggers PP’s exemption under Article 7(5)(a) and the safety valve under Article 7(12). For PET, the Commission has determined that the market can meet demand, and the exemption options are closed. PP’s challenge is an emerging market; PET’s challenge is an established market under pressure. PP or PET by 2030? The regulatory and supply asymmetry.